In recent years, the prominence of Blockchain technology has skyrocketed due to the growth of cryptocurrencies, like Bitcoin, Litecoin and Ethereum, by more than 1000%. Nevertheless, the benefits, functions and practical use cases of Blockchain extends well beyond its functionality as a cryptocurrency.

What is Blockchain?

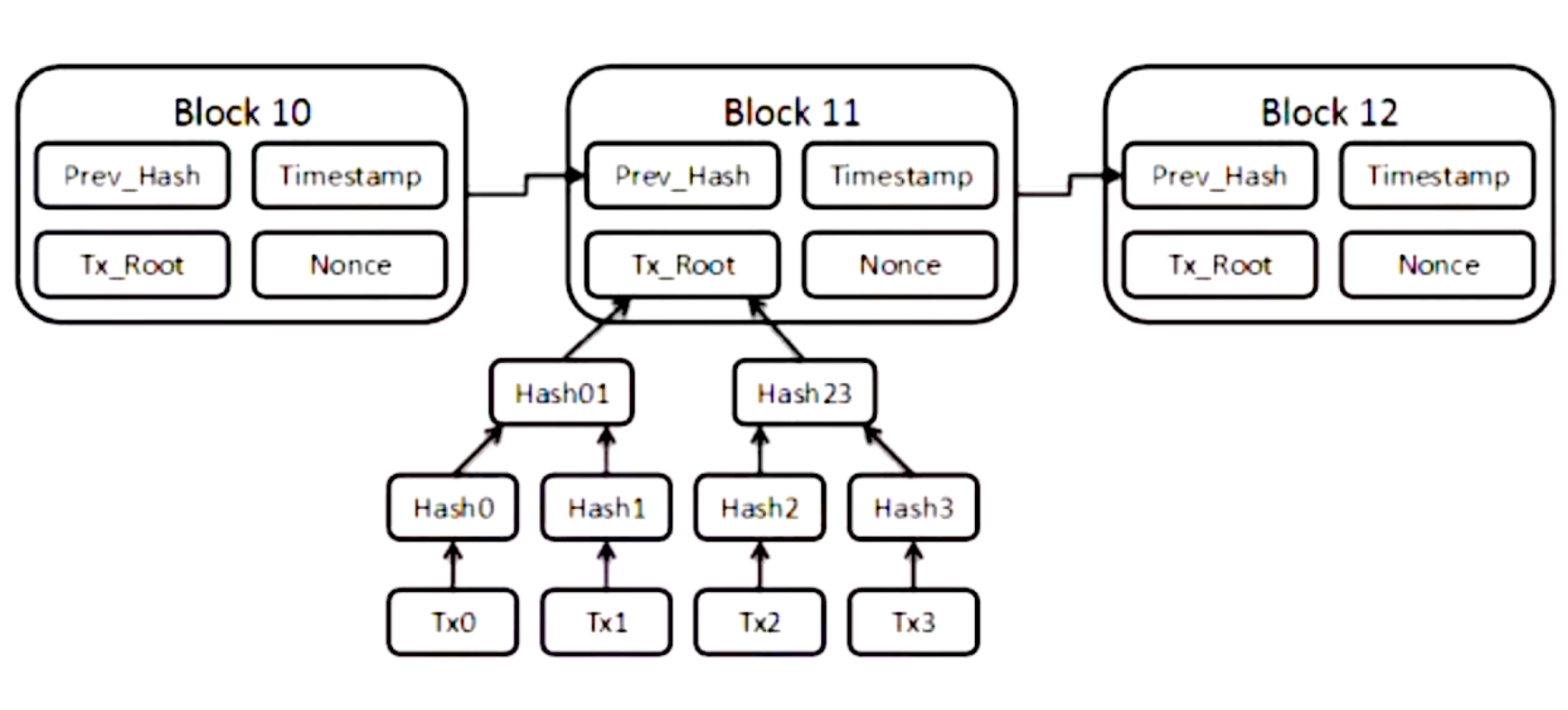

Blockchain is essentially a chain of blocks that contains data that are bundled together. It forms a distributed structure of data that is replicated and shared among the members of a network. This database is shared across a network of computers (distributed ledger network). Each block contains a record of many transactions. Each data block links to the previous block in the blockchain through a cryptographic hash of the previous block, a timestamp, and transaction data (usually represented as a merkle tree root hash), and a nonce.

How does a blockchain and blockchain network work? Adapted from Blockchains and Smart Contracts for the Internet of Things by Konstantinos Christidis and Michael Devetsikiotis.

- Users interact with the blockchain via a pair of private/public keys. They use their private key to sign their own transactions, and they are addressable on the network via their public key.The use of asymmetric cryptography brings authentication, integrity, and non-repudiation into the network. Every signed transaction is broadcasted by a user’s node to its peers. A node can generally act as an entry point for several different blockchain users into the peer-to-peer network.

- The neighboring peers make sure this incoming transaction is valid before relaying it any further; invalid transactions are discarded. Eventually this transaction is spread across the entire network.

- The transactions that have been collected and validated by the network using the process above during an agreed-upon time interval, are ordered and packaged into a timestamped candidate block. This is a process called mining. The mining node broadcasts this block back to the network.

- The nodes verify that the suggested block (a) contains valid transactions, and (b) references via hash the correct previous block on their chain. If that is the case, they add the block to their chain, and apply the transactions it contains to update their world view. If that is not the case, the proposed block is discarded. This marks the end of a round. Note that this is a repeating process.

Here are top 3 real-world applications and advantages of blockchain technologies.

1. Secure Digital Identities

Blockchain technology introduces a new and secure method to manage one's identity and record transactions in the digital world. These personal information is efficiently stored in the open, distributed, peer-to-peer ledger network. The decentralised nature of blockchain technology means that there is no centralised point of weakness, making it harder for hackers to exploit the system. This strengthens the system's security for protecting and managing digital identities.

Furthermore, blockchain technology allows users to have a verified and unique identity without the need to produce multiple official documents to validate their identities and profiles. Every account is unique because each digital identity has a single private and public key that is matched in the immutable (cannot be altered) ledger. This digital identity can store different online information securely on the blockchain.

One of the best use cases of blockchain is to provide secure digital identities for the billions of people who are unbanked (especially in developing nations). Many of them do not have easy access to banks and other financial services, but many of them have access to mobile phones. Giving a secure digital identity on the blockchain to these groups of people who are unbanked would allow them to gain access to financial services, enabling them to participate in the global economy.

2. Smart Contracts

Blockchain enables new digital relationships to be reliably secured and formed, through a smart contract.

"A smart contract is a computer protocol intended to digitally facilitate, verify, or enforce the negotiation or performance of a contract. Smart contracts allow the performance of credible transactions without third parties. These transactions are trackable and irreversible." - Wikipedia

How does a smart contract work? Adapted from Blockchains and Smart Contracts for the Internet of Things by Konstantinos Christidis and Michael Devetsikiotis.

1. Contract clauses are defined and business logic is coded into the contract. A properly written smart contract should describe all possible outcomes of the contract.

2. The relationship that Person A wishes to establish with his counter-parties driven by data. The transaction is a signed data structure (using the private key) authenticating a transaction. Person A deploys a smart contract that effectively says, ‘‘if you send this contract this data (5 units of Y), here’s how it will respond (1 unit of X)’’.

3. Hence, the smart contract is triggered by messages/transactions sent to its address.

4. A smart contract is deterministic; the same input will always produce the same output. If one writes a non-deterministic contract, when it is triggered it will execute on every node on the network and may return different random results, thus preventing the network from reaching consensus on its execution result.

5. A smart contract resides on the blockchain, and as such its code can be inspected by every network participant. This can be used to monitor for compliance.

6. Since all the interactions with the contract occur via signed messages on the blockchain, all the network participants get a cryptographically verifiable trace of the contract’s operations.

Emerging smart contract systems allow mutually distrustful parties to transact safely without trusted third parties. In the event of contractual breaches or aborts, the blockchain ensures that honest parties obtain commensurate compensation. - Adapted from Hawk: The Blockchain Model of Cryptography and Privacy-Preserving Smart Contracts, 2016 IEEE Symposium on Security and Privacy

Self-contracting protocols often contain self-executing and self-enforcing contractual clauses that can provide greater security, faster transactions and lower costs needed for contracting. By using smart contracts, contractual executions and digital agreements are no longer required to be validated by 3rd parties or intermediary authorities.

For example, smart contracts can become big disruptors in the insurance industry because it can change the way how insurance claims are processed. Smart contracts can reliably enable peer-to-peer insurance and risk-pooling, which would change the underwriting and risk analysis process of the insurance industry.

3. For Automated Governance

Over the last few years, many nations have started experimenting with implementing blockchain in regulating and governing the country. Blockchain technology essentially provides the government with a faster and more secure way to regulate various processes such as managing energy consumption data or issuing business identifications or even regulating a voting campaign.

According to Deloitte Gov, “blockchain’s influence in the public sector will be mostly behind the scenes. But the technology has the potential to bring security, efficiency, and speed to a wide range of services and processes.” Blockchain has many use cases in the public sector to improve the quality, efficiency and transparency of government services.